G7 government bonds? Check. Gold? Check. But that may not be enough as the coronavirus crisis accelerates a hunt for a wider pool of assets to better balance investment portfolios during stressful times.

Corporate and Chinese government debt are among alternatives being explored by multi-asset portfolio managers with mandates to invest across sectors, currencies and countries.

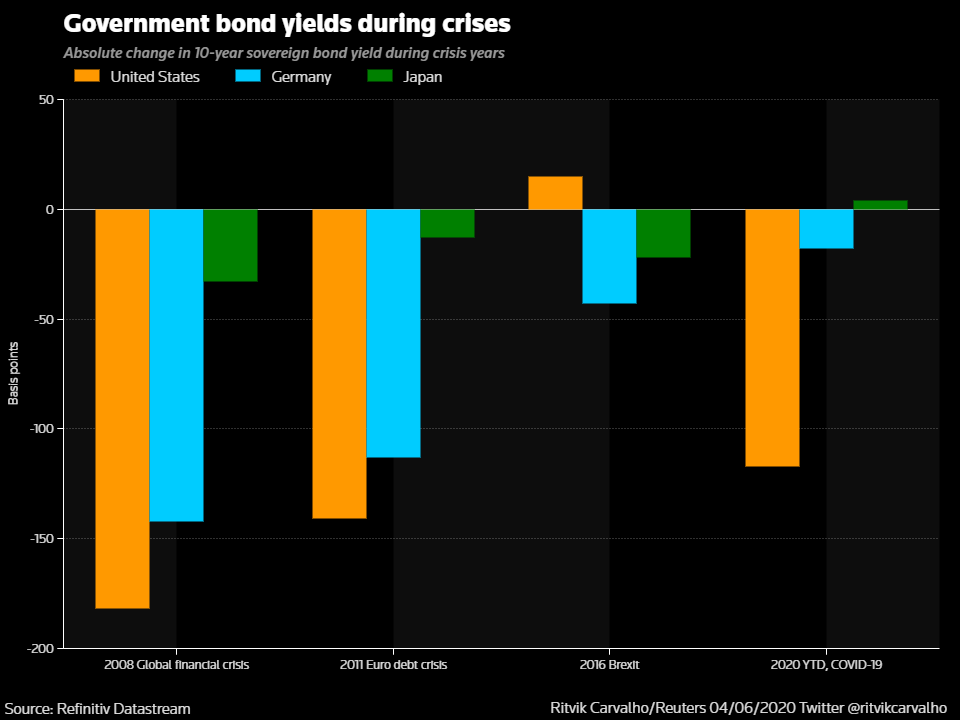

It’s been a moot point for years now whether U.S., Japanese and German bonds can adequately offset equity volatility. Given how relentlessly yields have fallen, many fear these bonds can no longer rally much when stocks fall - effectively losing the inverse correlation that made them a valuable defensive asset.

In fact Treasuries’ hefty rally in the recent crisis showed their safe-haven credentials remain intact. And U.S., German and other developed government bonds will always have a role as portfolio ballast, backed by conviction that these debts will never face default and can easily be bought or sold.

But the crisis has shown that even the safest of assets can succumb to panic — as global stocks tumbled during the volatile March 9-19 period, 10-year U.S. and German bond prices slid 9% and 7% respectively.

Compare that to Bunds’ 10% price rally during the worst of the 2011 euro debt crisis between end-May and early-August.

“We do have a sense that things are shifting,” said Wouter Sturkenboom, who helps to formulate investment strategy for $350 billion in client assets at Northern Trust Asset Management.

He has reallocated 7% of his equity portfolio towards U.S. corporate debt, inflation-linked bonds and cash, instead of government debt as he would have done earlier.

“You can’t just rely on (government bonds) in this environment, you need to go through the whole risk-control bucket,” Sturkenboom added.

Similarly, Gavin Counsell, a multi-asset fund manager at Allianz Global Investors, said he had roughly halved exposure to UK gilts since early March and favours precious metals.

The traditional multi-asset strategy - an equity-dominated portfolio alongside a big dollop of government bonds - appeared to function less well this year than during past crises.

During the 2008 global financial crisis for instance, a portfolio comprising equity and government bonds in a 60:40 ratio would have lost 2%. But in March-April this year, a similar portfolio lost 13%, according to investment advisory firm BCA Research.

The reason bonds find it harder to move inversely to equities is that German and U.S. 10-year yields are 500 bps and 350 bps lower than they were on the eve of the 2008 crisis.

“A stronger cross-asset correlation is the worst nightmare for any portfolio manager, and this has been a defining feature of this crisis, prompting the search for alternative assets,” said Dhaval Joshi, chief European strategist at BCA.

ALTERNATIVE?

Luckily for investors, the U.S. Federal Reserve’s decision to include company debt in its stimulus programme has sharply expanded the pool of potential ‘safe’ assets, adding $7 trillion in top-rated corporate bonds to the existing $20 trillion in government debt, Fed and IHS Markit data show.

In Europe too, $2.4 trillion of top-rated credit is eligible for European Central Bank purchases - on top of $8 trillion in government debt.

Investors pumped a record $20.8 billion into investment grade corporate bonds in the week to June 3, according to BofA.

“Investment-grade paper ... is the new Treasuries as it has the backing of the Fed,” said Jack McIntyre, fixed income portfolio manager at Brandywine Global.

“I would bypass some of these traditional safe haven markets to buy (IG) debt. Treasuries have an explicit guarantee from the government but IG credit has an implicit guarantee from the Fed.”

Some are casting their net wider.

Stuart Rumble, an investment director at Fidelity Investments is exploring Chinese government bonds as a diversification strategy - noting their lower correlation to global equities.

They also pay a reasonable income - at 2.8% for 10-year paper they provide a 250-300 bps pickup over U.S. and European debt.

BlackRock’s head of Asian Credit, Neeraj Seth, predicts a greater shift towards Chinese debt for portfolio diversification.

While emerging market bonds usually move in line with equities and other risk assets, Chinese government bonds increasingly go in the other direction - behaving like Treasuries or Bunds.

In the first quarter of 2020, they gained nearly 5%, contrasting with a 15% drop in emerging market bonds. They have also outperformed U.S. Treasuries and German Bunds this year on a volatility-adjusted basis, Refinitiv data shows.

What about parking cash in money market funds?

Investment advisers say that in countries such as Germany where one literally pays to hold cash, even conservative investors are increasingly willing to deploy the cash in equities and use option hedges to protect those positions.

“I had a call last week with a traditional German family office CEO who has never used options,” said Christian Mueller-Glissmann, managing director of portfolio strategy and asset allocation at Goldman Sachs.

“And he essentially said it’s time to start talking about put options.”

This article originally appeared on Reuters.