(Peter Mauthe, Flexible Plan) Personal biases influence how people interpret events and what they experience emotionally. For example, there will always be a bullish, bearish, and neutral way to interpret the news that the financial markets are faced with every day. Which one is correct? Who can say?

As a portfolio manager, Flexible Plan views the news of the day, week, or month objectively and agnostically. We are not concerned with “being right in our view.” We are concerned with being on the right side of the trend of each of the markets (stock, bond, alternative) in which we participate.

What that means is that while individually we may have opinions about the state of the economy or who is elected to office, those opinions have no bearing on how we make investment decisions. Instead, we are focused on the data, rule sets, and results that help guide us to being invested on the correct side (long, inverse, cash) of all markets.

Our rules-based investing at work in the real world

Let’s examine how Flexible Plan’s rules-based investing has performed in a couple of real-world examples.

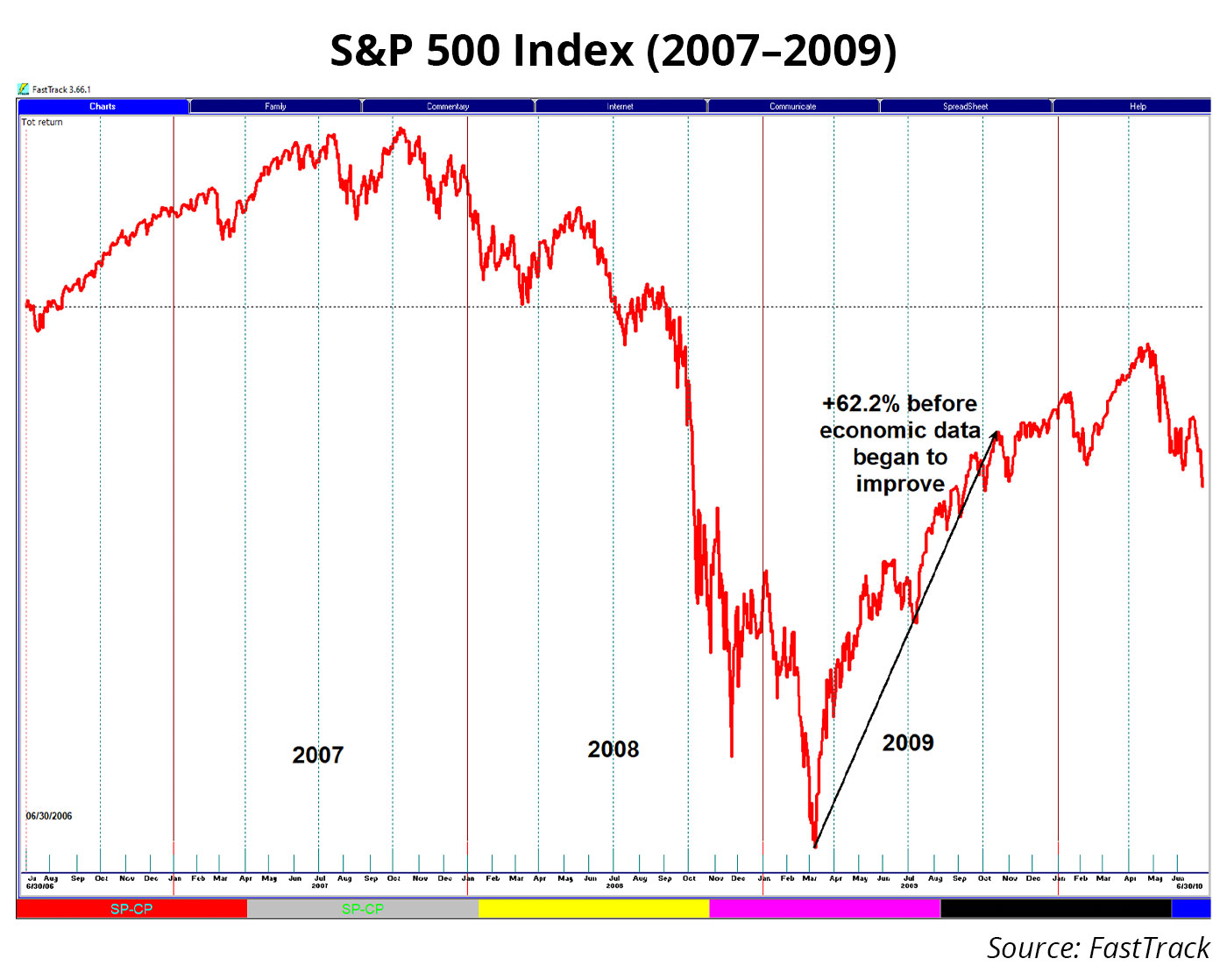

First, let’s take a look at the 2007–2009 financial crisis. The following graph illustrates the S&P 500 during that period. Stocks began deteriorating in late 2007 and early 2008, while the economy (by all news headline accounts) was still apparently healthy. Nonetheless, our strategies, following a predetermined set of rules, generally took action to reduce exposure to stocks even though the economic news at the time was quite good.

In 2009, in the heat of the financial crisis, stocks began moving higher while the economic news and data were appallingly bad. However, our rules-based strategies generally responded appropriately and increased equity exposure as stocks moved higher.

In late 2009, the economic news began to improve, validating what the markets and many of our rules-based strategies recognized much earlier in the year.

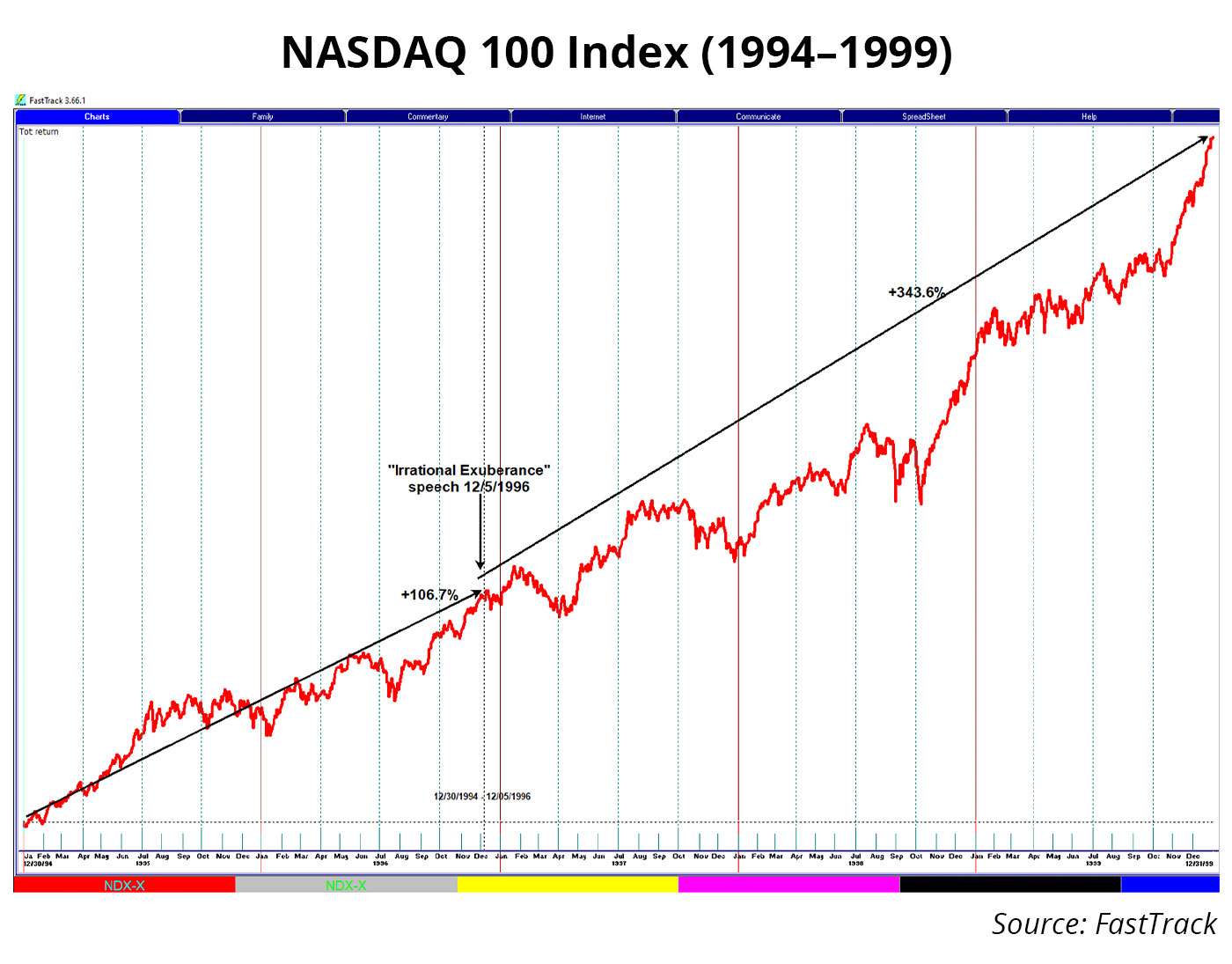

Now let’s take a look at another memorable example from the late 1990s. In late 1996, following a significant move up in the stock market (as measured by the NASDAQ 100 Index), then Chairman of the Federal Reserve Board Alan Greenspan gave a speech in which he referred to investors as having “irrational exuberance.” Based on many historical measures, he was right, and the stock market corrected for several days thereafter. Stocks then advanced significantly higher over the next three-plus years.

While the chairman arrived at his conclusion about stocks being overpriced based on historical perspective and a personal interpretation of investor behavior, Flexible Plan relied on data that indicated that stocks were moving higher and generally invested according to the various objective rules sets deployed. Our rules-based methods do not rely on personal bias (decidedly subjective information)—they rely on data. They analyze whether prices are going up, down, or sideways; whether they are volatile; and how closely correlated they are among themselves.

None of the objective calculations made by Flexible Plan strategies or the actions they generate depend on the news headlines of the day—or anyone’s interpretation of them. Rather, they depend on data derived from the markets’ responses to the news or, more importantly, their anticipation of the news, as often happens.