(Beaumont Capital) The Fed’s dot-plot update and more-hawkish-than-expected turn took the markets off guard this week as investors prepare for two rate hikes in 2023.

Sparked by significant increases to GDP and inflation forecasts through the end of the year, the announcement kicked off a flurry of activity in the markets including a jump in treasury yields, the largest two-day tightening of spreads since March of 2020, and a pivot away from inflation-sensitive sectors.

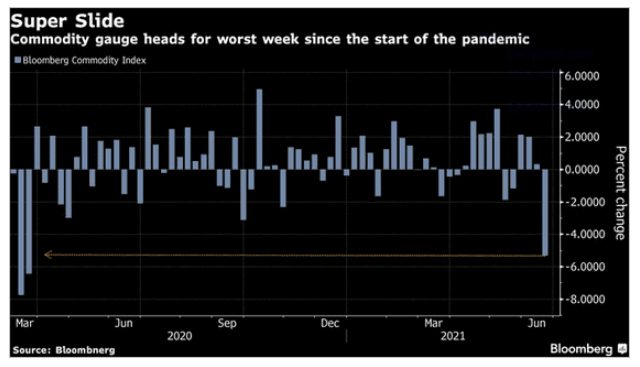

The Fed has remained consistent in their view that significant inflation will be a temporary phenomenon though, and their position appears supported by the commodities market which is off highs as prices slide and appear to be moving toward their worst week since the onset of the Covid-19 crisis.

Will energy be the exception though as gasoline demand rebounds and U.S. oil production breaks above its pandemic-era range?

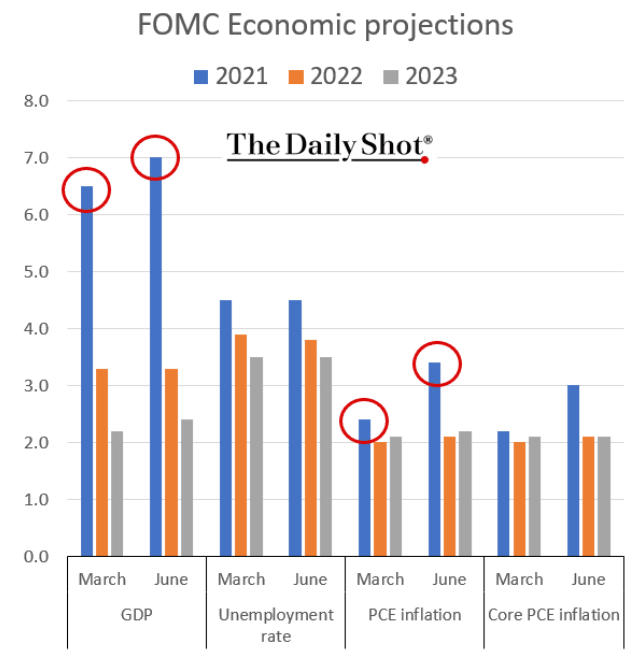

1. While the Fed kept to their transient inflation view, some seemed surprised that they are expecting to raise rates in 2023. The have indicated so for years…

Source: The Daily Shot, from 6/17/21

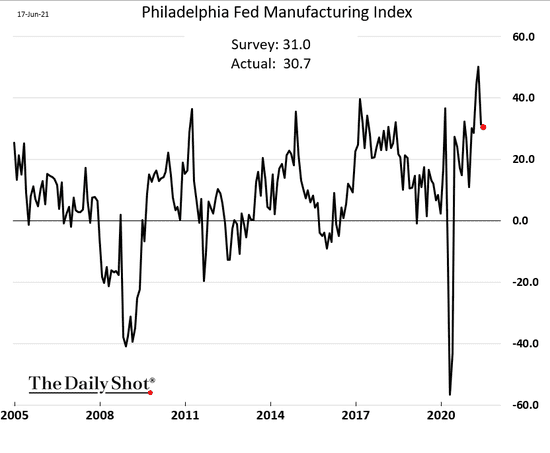

2. The NY and Philly Fed’s manufacturing reports showed moderation, but still solid growth:

Source: The Daily Shot, from 6/18/21

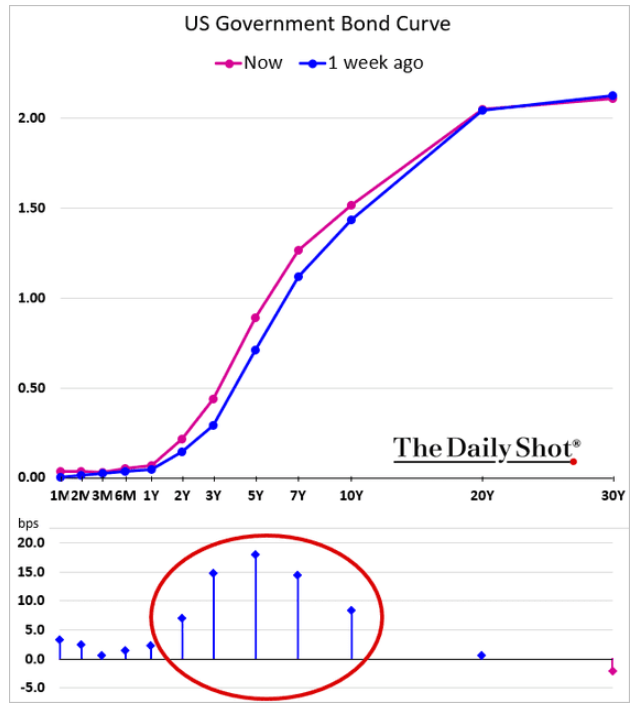

3. All the markets; stocks, bonds, currencies and commodities, are digesting the Fed’s news. The Fed has been remarkably consistent so the rate news was, well, not news at all. But to those who didn’t believe them, reactions abound.

Source: The Daily Shot, from 6/18/21

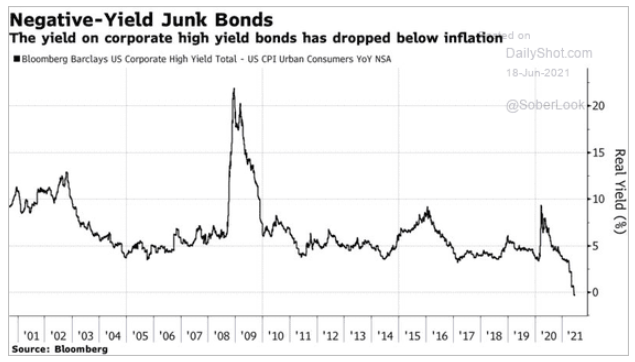

4. Real rates on junk bonds are negative? Calm junk bond markets are usually a good sign for equities, but is this becoming a bubble?

Source: Bloomberg, from 6/18/21

5. Most commodities are retreating after a parabolic rise. Where to from here?

Source: Bloomberg, from 6/18/21