The market still seems to be nursing a post-Federal Reserve hangover, though seemingly because of too little rather than too much liquidity the central bank said it would add to the proverbial punchbowl.

But the bigger picture in markets is the performance of the technology sector. Even with losses in seven of the past 10 sessions, the Nasdaq Composite through Thursday had still gained nearly 22% in the midst of a pandemic, and bounced 59% off its March lows. This week’s strong demand for initial public offerings from the likes of Snowflake show demand for technology stocks is still there.

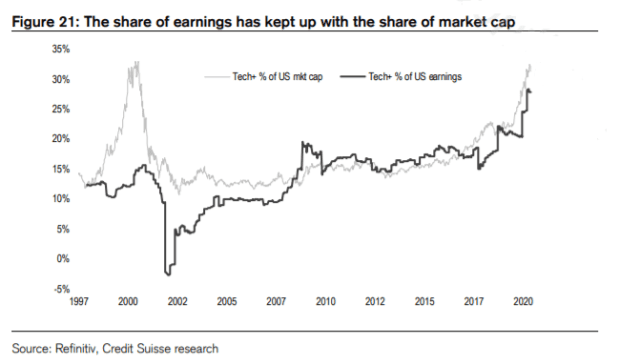

Strategists at Credit Suisse say the word “bubble” isn’t appropriate for the tech sector. Technology investment share of gross domestic product, and capital expenditure to sales, are only slightly above their norms, and forecast revenue growth is in line with trends, they say. The London-based team, led by Andrew Garthwaite, adds that, during bubbles, price-to-earnings ratios tend to widen out to 45 to 72 times earnings; the Nasdaq right now is on 37 times earnings.

But even if they don’t apply the word “bubble,” the Credit Suisse strategists do concede there are risks. In software, the ratio of price to sales is elevated, and the top five stocks now represent 26% of market capitalization, which is nearly as high as the 30% in Japan in 2000. A vaccine for COVID-19 may boost sectors most sensitive to the virus, such as financials, real estate and leisure, and that would be a negative for tech. Another big threat is on the regulation front — and not so much antitrust but taxes. A sales tax of 4%, which is similar to proposals made in France and the U.K., would take 20% off profits.

| Company | Estimated impact on 2022 earnings from 4% sales tax |

| Microsoft | -10.2% |

| Apple | -16.1% |

| Amazon | -49.6% |

| -10.7% | |

| Alphabet | -17.5% |

The Credit Suisse strategists highlight SAP and Microsoft as software stocks they like. Excluding stock-based compensation, Microsoft has a free cash flow yield of 2.6% this year, and SAP is on 2.3%. Software also has the advantage of having defensive characteristics, as companies try to cut costs by automating. SAP’s U.K. business experienced double-digit growth in the quarters following the Brexit vote, and its oil and gas-related business had its strongest quarter when the oil price fell below $30 per barrel in 2016.

Ericsson is their top telecom equipment pick for the move into 5G, with rivals Huawei and ZTE effectively phased out by U.S. scrutiny of the Chinese companies. Only 5% of smartphones are 5G, Credit Suisse points out. In semiconductors, they highlight ASML and Taiwan Semiconductor Manufacturing for their “natural monopolies,” as well as Samsung Electronics. Credit Suisse also is positive on China internet/tech names, even with the tough U.S. rules, highlighting Tencent and Alibaba.

The strategists are neutral on Apple, as the Credit Suisse team point out the size of Apple’s addressable market are those making at least $12,000 a year, amounting to a market cap of $1,680 per head for those 1.25 billion people. That requires $560 in spending per person, which “appears ambitious, even if 15%-20% of Apple’s revenue are corporate customers.”

Credit Suisse also struggles to justify Tesla’s market cap representing 64% of the rest of the global automobile sector. But neither Google owner Alphabet nor Facebook looks expensive on earnings relative to the market, and both look attractive when comparing their free cash flow yield to the 10-year Treasury.

This article originally appeared on MarketWatch.