(Marta Norton, Morningstar) Reviewing their financial positions for the year ahead has many investors worried, which is a natural reaction. Risk abounds in 2022—from inflation, to rising interest rates, to lofty valuations. How do we adjust our mindset to ride out the potential rough times to come? It helps to keep our goals in mind, remember to adopt the long view over the short one, and consider the wisdom of Warren Buffett:

"In the 20th century, the United States endured two world wars and other traumatic and expensive military conflicts; the Depression; a dozen or so recessions and financial panics; oil shocks; a flu epidemic; and the resignation of a disgraced president. Yet the Dow rose from 66 to 11,497."

Buffett has enjoyed a long record of success, and he didn't create such value by letting immediate concerns and fears alter his approach– nor should you.

The future is unknowable, so the best we can do is to address it in terms of probability and preparation. In assessing probability, however, people are often driven by bias and emotion, emphasizing the positive at one moment and the negative at another. That narrow emphasis is likely to be reflected in the rapid changes in price of investments. Over-emphasis on optimism or pessimism leads to price volatility, which is part of being an investor, and enduring volatility is a price we pay for reaching our goals.

One must learn to ride out volatility and avoid giving in to pessimism about risk in the short term. After all, if we allow pessimism to drive us into selling during a downturn, we lock in a loss when we might otherwise have stayed the course and watched our fortunes reverse themselves.

That's not to say the fair value of an asset cannot drop. It can, and when that happens, previous valuation estimates no longer apply. That's why we pay close attention to the economic fundamentals of an asset and price it accordingly. That's investment rather than investor risk.

Do downturns occur? They do—and have done so repeatedly. In fact, we've seen the S&P 500 fall by 10% or more 54 times since 1980 alone.

Risk in the Small Versus Risk in the Large

That's why it's important for investors to reflect on their own experience with risk. One helpful way of doing so is to distinguish between risk in the small versus risk in the large. Risk in the small is how we react to volatility. This is a sensitive area that provokes emotions such as fear and greed, often to our own detriment. Risk in the large is all about long term goals and doing what it takes over time to avoid shortfalls. Most of us know that we must accept some investment risk to reach our desired financial goals.

This way of differentiating risk isn’t new, but it can make a difference, as investors can be significantly better at managing risk in the large (goal attainment) than risk in the small (panicked selling amid volatility). Regarding the latter, the evidence overwhelmingly shows that people tend to act in downturns, mostly to their detriment, with outflows from their portfolio during bouts of volatility. Refocusing attention to think in terms of long-term investing, and to focus on overarching goals, can be a useful antidote to the bad behaviors investors can succumb to in the face of unavoidable volatility.

We don’t believe investors need to give in during periods of perceived risk; instead, we can address it and prepare for it. That’s where true downside protection comes in, starting with goals and working our way down to robustness.

Our definition of investment risk (the ‘permanent loss of capital’) is likely the same as yours. We seek to understand risk across the full array of potential outcomes, ensuring that a portfolio has the ability to withstand or overcome adverse conditions.

Investing involves its fair share of adverse conditions, but people seldom talk about having a robust portfolio. Diversified, maybe, but not robust. To us, robustness can be considered in line with this quote from American author and professor John A. Shedd: " A ship in harbor is safe, but that is not what ships are built for."

We believe one of the best ways to control for risk is to buy fundamentally strong investments with attractive valuations. But of equal importance is having different risk and return drivers that can weather unpredictable storms to maximize the likelihood of achieving your goals. This can conceptually be applied in a multi-asset portfolio, or when combining multiple portfolios together (achieving more than the sum of the parts).

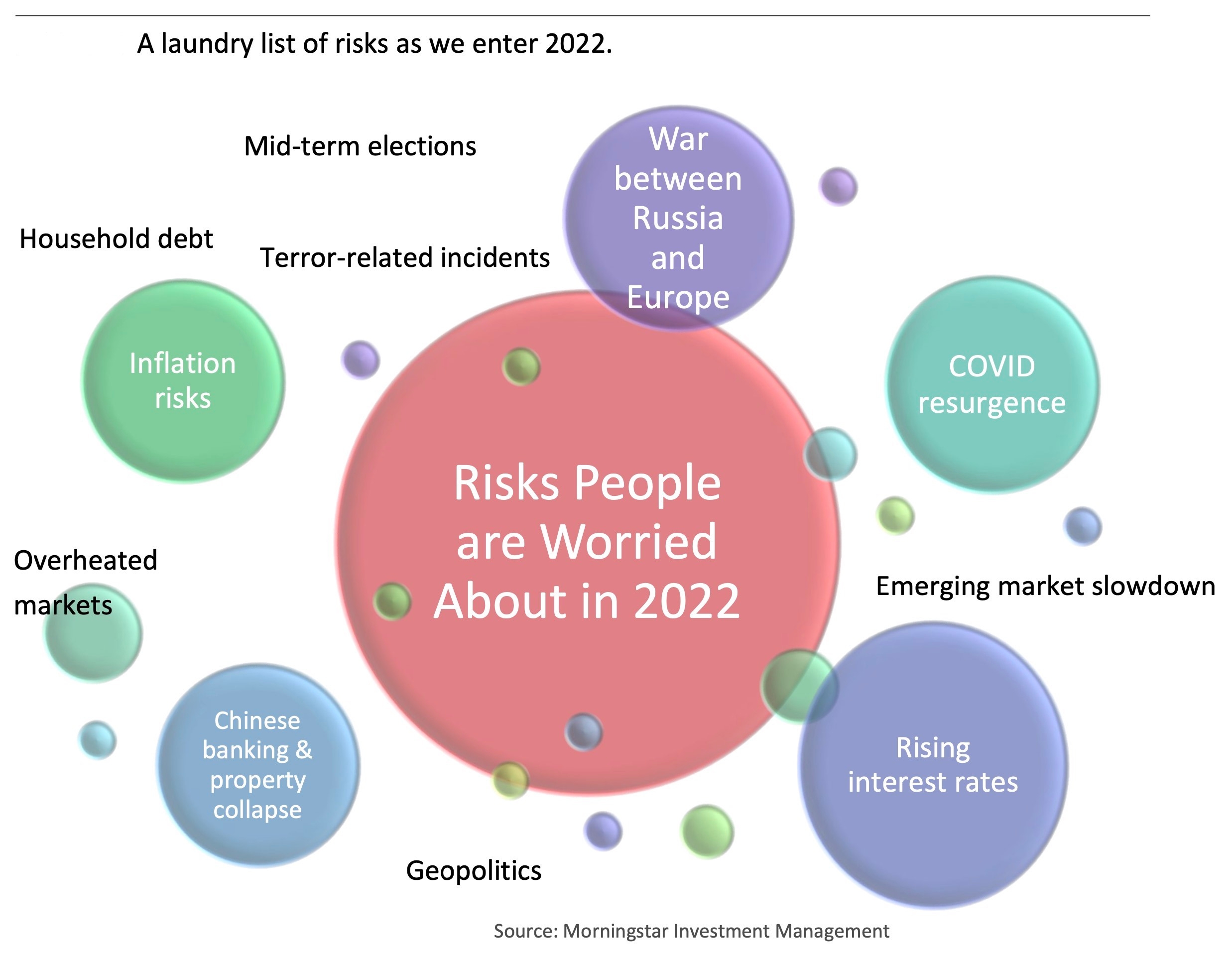

How Would the Average Investor Summarize the Key Risks in 2022?

Let's now get practical and apply this to the 2022 landscape. The below infographic presents a decent capture of the key event risks and fundamental risks investors face as we enter 2022. We will otherwise re-label them as the reasons most people are scared to invest.

Of course, any one of these risks could materialize into a market setback, and no investment loss is good for an investor. This is especially the case for investors with shorter time horizons or those nearing retirement. (Sequencing risk means a big investment loss at the start of retirement and this can have a material impact on income levels from that point on.) But that doesn't mean we should run for cover every time new risks surface.

Investor behavior isn’t always rational, and people tend to approach markets with overconfidence and a vividness bias. This tends to really show itself at extremes, and especially in down markets.

Practical suggestions to alleviate anxiety about investment losses can be found in the field of decision sciences. Perhaps one of the easiest and most powerful ways is to simply reaffirm your goals before making any decisions. From a behavioral standpoint, people may be more successful when assessing risk in the large, and that reframing can act as a stabilizer.

Another is to look at your portfolio under the lens of robustness. If you take comfort that your portfolio can stand up to many different scenarios (think all-weather) then accepting some volatility is much more palatable and a pre-requisite for good returns.

Opinions expressed are as of the current date; such opinions are subject to change without notice. Morningstar Investment Management shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions or their use. This commentary is for informational purposes only. The information, data, analyses, and opinions presented herein do not constitute investment advice, are provided solely for informational purposes and therefore are not an offer to buy or sell a security. Please note that references to specific securities or other investment options within this piece should not be considered an offer (as defined by the Securities and Exchange Act) to purchase or sell that specific investment. Performance data shown represents past performance. Past performance does not guarantee future results. All investments involve risk, including the loss of principal. There can be no assurance that any financial strategy will be successful. Morningstar Investment Management does not guarantee that the results of their advice, recommendations or objectives of a strategy will be achieved. This commentary contains certain forward-looking statements. We use words such as “expects”, “anticipates”, “believes”, “estimates”, “forecasts”, and similar expressions to identify forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason. Past performance does not guarantee future results. Morningstar® Managed PortfoliosSM are offered by the entities within Morningstar’s Investment Management group, which includes subsidiaries of Morningstar, Inc. that are authorized in the appropriate jurisdiction to provide consulting or advisory services in North America, Europe, Asia, Australia, and Africa. In the United States, Morningstar Managed Portfolios are offered by Morningstar Investment Services LLC or Morningstar Investment Management LLC, both registered investment advisers, as part of various advisory services offered on a discretionary or non-discretionary basis. Portfolio construction and on-going monitoring and maintenance of the portfolios within the program is provided on Morningstar Investment Services behalf by Morningstar Investment Management LLC. Morningstar Managed Portfolios offered by Morningstar Investment Services LLC or Morningstar Investment Management LLC are intended for citizens or legal residents of the United States or its territories and can only be offered by a registered investment adviser or investment adviser representative. Investing in international securities involve additional risks. These risks include, but are not limited to, currency risk, political risk, and risk associated with varying accounting standards. Investing in emerging markets may increase these risks. Emerging markets are countries with relatively young stock and bond markets. Typically, emerging-markets investments have the potential for losses and gains larger than those of developed-market investments. A debt security refers to money borrowed that must be repaid that has a fixed amount, a maturity date(s), and usually a specific rate of interest. Some debt securities are discounted in the original purchase price. Examples of debt securities are treasury bills, bonds and commercial paper. The borrower pays interest for the use of the money and pays the principal amount on a specified date. The indexes noted are unmanaged and cannot be directly invested in. Individual index performance is provided as a reference only. Since indexes and/or composition levels may change over time, actual return and risk characteristics may be higher or lower than those presented. Although index performance data is gathered from reliable sources, Morningstar Investment Management cannot guarantee its accuracy, completeness or reliability. The concept of an economic moat plays a vital role not only in our qualitative assessment of a firm’s long-term investment potential, but also in the actual calculation of our fair value estimates. An economic moat is a structural feature that allows a firm to sustain excess profits over a long period of time. We define excess economic profits as returns on invested capital (or ROIC) over and above our estimate of a firm’s cost of capital, or weighted average cost of capital (or WACC). Without a moat, profits are more susceptible to competition. We have identified five sources of economic moats: intangible assets, switching costs, network effect, cost advantage, and efficient scale. Companies with a narrow moat are those we believe are more likely than not to achieve normalized excess returns for at least the next 10 years. Wide-moat companies are those in which we have very high confidence that excess returns will remain for 10 years, with excess returns more likely than not to remain for at least 20 years. The longer a firm generates economic profits, the higher its intrinsic value. We believe low-quality no-moat companies will see their normalized returns gravitate toward the firm’s cost of capital more quickly than companies with moats. To assess the direction of the underlying competitive advantages, analysts perform ongoing assessments of the moat trend. A firm’s moat trend is positive in cases where we think its sources of competitive advantage are growing stronger; stable where we don’t anticipate changes to competitive advantages over the next several years; or negative when we see signs of deterioration. All the moat and moat trend ratings undergo periodic review and any changes must be approved by the Morningstar Economic Moat Committee, comprised of senior members of Morningstar’s equity research department. Index Information Individual index performance is provided as a reference only. Each index is unmanaged and is not available for direct investment. Since indexes and/or composition levels may change over time, actual return and risk characteristics may be higher or lower than those presented. Although index performance data is gathered from reliable sources, we cannot guarantee its accuracy, completeness or reliability. Index data sources are as follows. S&P 500 Index—An index of 500 stocks chosen for market size, liquidity and industry grouping, among other factors. The S&P 500 is designed to be a leading indicator of U.S. equities and is meant to reflect the risk/return characteristics of the large cap universe. The S&P 500 is a market value weighted index. MSCI EAFE Index (Europe, Australasia, Far East)—A free float-adjusted market capitalization index designed to measure the equity market performance of developed markets, excluding the U.S. & Canada. Bloomberg Barclays U.S. Aggregate Index—A market value weighted performance benchmark for investment-grade fixed-rate debt issues, including government, corporate, asset-backed, and mortgage-backed securities, with maturities of at least one year. MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets