(Forbes) Goldman Sachs and JPMorgan are top of the largest investment banks in the world. Since the recession, Goldman Sachs has transformed itself from an investment bank heavily focused on securities trading to a bank holding company with diversified streams of revenues like Asset & Wealth Management and Investing & Lending. Despite notable changes to its business model, Goldman continues to report the highest advisory & underwriting fees (also known as investment banking revenues) among all global investment banks thanks to its unrivaled strength in the global merger & acquisition (M&A) advisory industry. However, JPMorgan has also done extremely well over recent years to boost its investment banking fees and has been hot on Goldman’s heels over recent years owing to its leadership in the global debt origination market. Notably, JPMorgan’s investment banking revenues were higher than Goldman’s in 2016, and we believe JPMorgan beat Goldman to the #1 position again in 2019.

Trefis captures trends in the investment banking business for Goldman Sachs and JPMorgan in a detailed interactive dashboard, parts of which are summarized below. While Goldman Sachs has a larger presence in M&A advisory and equity underwriting, it is trailing JPMorgan by a significant margin in the debt origination market.

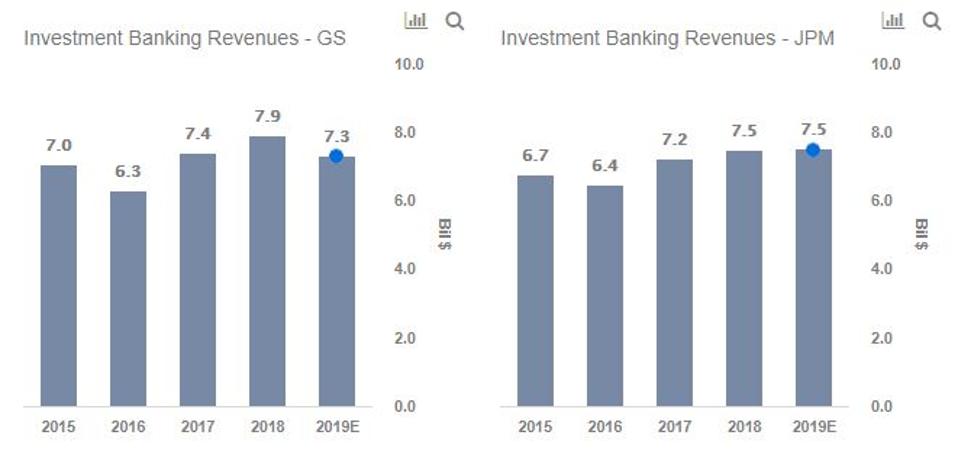

Goldman has reported higher revenues in 3 of the last 4 years, with JPMorgan edging ahead in 2016 and very likely in 2019 too

- Although Goldman Sachs has reported higher investment banking revenues than JPMorgan over the last 4 years (barring 2016), the difference is not significant.

- Goldman’s investment banking business is bigger in terms of M&A advisory and equity underwriting deal volumes. However, JPMorgan is way ahead of its peer in the Debt Origination business.

- In terms of average growth over the last 4 years, Goldman is again slightly ahead of its peer, growing at an average annual rate of 4.5% as compared to the 3.7% of JPMorgan.

- Going forward, we expect JPMorgan’s investment banking revenues to be around $7.5 billion for 2019 (marginally higher than the 2018 figure), which should help it surpass Goldman’s expected revenue figure of $7.3 billion (down 7% y-o-y).

- This decline of 7% in Goldman’s investment banking revenues would have been driven by lower equity underwriting deal volume and negative growth in debt origination deal volume.

Investment banking contributed more than 21.5% to Goldman Sachs’ revenues in 2018, which was more than 3x the segment’s contribution to JPMorgan’s top line

- Goldman Sachs investment banking has averaged around 21% of total revenues, while JPMorgan’s figure was one-third of its peer – around 7% of total revenues.

- This implies that Goldman Sachs is heavily dependent on the investment banking business, as compared to its peer, which has a much more diversified business model with a huge consumer as well as custody banking presence.

Goldman’s M&A deal volume is significantly higher than its peer, so is its revenue per dollar of deal volume.

- Goldman’s M&A deal volume was almost 48% more than its peer in 2015. However, the difference has gradually reduced over the last 4 years, from 48% to 20% in 2018.

- Both the banks witnessed a slump in M&A deal volume in 2017, due to overall low M&A activity in the year.

- Goldman Sachs has reported slightly higher fees as % of M&A deal volume than JPMorgan over each of the last four years.

- This implies that Goldman is generating higher revenue per dollar of M&A deal volume as compared to its peer.

- Goldman Sachs is the market leader in the global M&A advisory industry, with M&A advisory revenues of $3.5 billion in 2018 – 40% more than JPMorgan’s figure of $2.5 billion.

Although Goldman has managed higher equity underwriting deal volume over the recent years, JPMorgan has generated higher revenue per dollar of deal volume.

- Equity underwriting deal volume is the total value of Initial Public Offering or Follow-On Public Offering deal. The bank earns its fees as a % of the total deal value.

- Goldman’s equity underwriting deal volume was $64.9 billion in 2018 which was 17% more than its peer. It has reported a higher figure than JPMorgan for each of the last 4 years, barring 2016.

- Although fees as % of equity underwriting deal volume have increased for both the banks over the last 3 years, JPMorgan’s figure of 3.04% in 2018 was 1.2x that for its peer.

JPMorgan has higher debt origination deal volume, although its fees income per dollar of deal volume is lower than its peer

- JPMorgan is the market leader in the debt underwriting space and is expected to retain its position for the foreseeable future.

- JPMorgan’s debt origination deal volume was $369.9 billion in 2018 which was 52% more than its peer. Further, it has reported a significantly higher figure than Goldman for each of the last 4 years.

- Goldman has generated higher fees income per dollar of debt origination deal volume over the last 3 years.

Conclusion

- Although Goldman Sachs has a larger investment banking business both in terms of M&A advisory and equity underwriting deal volume, it is trailing JPMorgan in the debt origination space.

- Further, JPMorgan has generated more fees income per dollar of equity underwriting deal volume. On the other hand, Goldman has delivered better returns on debt origination as well as M&A advisory activities going by fees per dollar of deal volume.

- JPMorgan has diversified revenues streams with investment banking business contributing almost 7% of total revenues over the last decade. On the other hand, Goldman Sachs is more dependent on investment banking business which accounted for more than 18% of its revenues.

- Finally, the difference in investment banking revenues for both banks is quite small, and given JPMorgan’s lead in debt origination space and its better returns on equity underwriting deals, JPMorgan could consistently generate more investment banking revenues compared to Goldman Sachsin the long run.