(Fortune) - The dot-com crash haunts the memories of many of the more seasoned investors on Wall Street, and this year’s stock market rout is conjuring up some serious déjà vu.

The S&P 500 is down 19% since the start of the year, and the tech-heavy Nasdaq has fared even worse, plummeting over 28%.

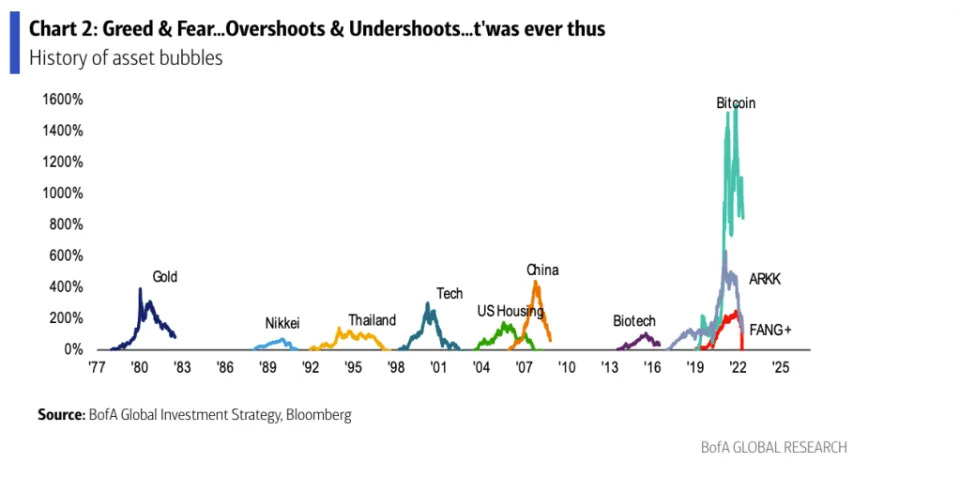

But we could be just halfway through the stock market decline based on historical trends. Between March 2000 and October 2002, the Nasdaq-100 sank 78% as once-loved, but largely unprofitable, tech firms fell by the wayside.

It was a dot-com bust that washed out a slew of tech sector darlings that had ruled the 90s, and there’s a startlingly similar trend today in a market that didn’t exist decades ago—cryptocurrencies. The crypto market has lost roughly $1 trillion in value year-to-date in one of the worst sell-offs in the maturing market’s history.

It’s part of a dramatic drop in risk assets that has some of the world’s most prominent investors, including Jeremy Grantham and Scott Minerd, arguing we’re reliving the blow-up of the dot-com bubble.

They say that the speculative nature of many investments in the market over the past few years shows that not much has changed since 2000.

“There's a very strong similarity between the dot-com crash and the bear market that we're experiencing today,” George Ball, the chairman of Sanders Morris Harris, a Houston-based investment firm that manages $4.9 billion, told Fortune. “You would have thought that investors, broadly, professional or retail, would have learned their lesson in 2000. And yet, something eerily alike has happened.”

And, of course, what followed the dot-com bubble bursting was a short but painful recession. Is that where markets are headed now?

Another growth over profits era

Former Fed Chair Alan Greenspan famously described dot-com-era investors and markets as “irrationally exuberant,” and the 2010s clearly played host to a similar dynamic.

Both eras were marked by a growth-over-profits mentality on Wall Street and an aggressive proliferation of retail investing. And in both periods of economic expansion, the best-performing stocks belonged to growth-focused companies.

Take the example of Priceline. In 1999, the online travel agency became an overnight success, going public just over a year after its founding. The company quickly racked up $142 million in losses in its first few quarters in business after spending millions on advertising using Star Trek star William Shatner, but that didn’t matter to investors.

All they wanted was a piece of rapid growth from a company that was set to make travel agents a thing of the past. Shares soared from the $96 IPO price (adjusted for a six-to-one reverse stock split) to nearly $1000 at one point, but when the market turned, the stock fell 99% to a low of just $6.60 by October 2002.

For a parallel today, consider Peloton. The workout bike maker became a work-from-home darling during the pandemic, causing its stock to soar over 600% from March to December 2020, even as it posted consistent losses. Of course, the stock eventually cracked, with shares falling over 90% from their record high as investors reconsidered whether the workout bike company was really worth nearly $50 billion (its peak market cap).

It’s clear investors in both the dot-com era and today have been willing to pay up for market share gains and potential future earnings, even in business models that have yet to prove themselves capable of turning a profit, according to Ball.

“In the dot-com era, and in the current market run-up and decline this year, there was a fervent, largely mindless belief that a subset of investments would go up in price forever,” he explained. “The reasoning, if there was any, had no grounding in metrics, no real grounding in logic, and relied on a very high rate of growth continuing beyond any reasonable expectations of the boundaries of scale.”

Ball added that the “poisons” that ultimately led to a crash then are the same as what markets are currently experiencing.

Dr. Bryan Routledge, an associate professor of finance at Carnegie Mellon University, told Fortune that the dot-com blowup ended up being a proving ground for new business models, and that we may experience something similar today.

“What you see in bear markets and what you see in recessions is that some of these ideas that have not yet been sort of battle-tested are exposed. That’s an analogy to the dot-com era, lots of companies just lost it, their model wasn't robust,” he said.

Tech stocks and crypto: dot-com darlings 2.0

In the run-up to the dot-com bubble, any company that attached “.com” to its name seemed to almost immediately find success, and it’s been the same with “crypto” and “DeFi” recently.

Investors have flocked to these new technologies. The logic, both then and now, went something like this:

“Something's growing very rapidly; it will always grow at a very rapid rate. The greater fools theory then takes over, people use leverage, and then at the extreme growth cannot be maintained, the leverage is exposed, and the crash comes about,” Ball said. “That's certainly true today in tech stocks, it's been true in crypto, as you know, and it was particularly evidenced by the price declines in completed SPACs.”

The similarities between the two eras have Ball concerned that, even after tech stocks’ recent collapse, more pain could be ahead for investors.

“People don't want to admit it, but psychology has the biggest impact on stock prices, much more than the economy, much more than earnings. It is psychology, and the psychology has turned negative,” he said, adding that he expects the Nasdaq could “quite possibly” dip below $10,000 this year, or roughly 12% from Friday’s close, but “no one knows where the tech bottom is going to be.”

“I'd be much more apt to buy tech stocks when they start going up again rather than trying to figure out how low they are going to go, or catch the falling knife. When psychology and tech stocks start to go up, that's probably the right moment to get invested,” Ball explained.

Still, not everyone is so pessimistic about the future of tech shares.

Liz Ann Sonders, Charles Schwab & Co.’s chief investment strategist, noted in a Wednesday tweet that the S&P 500 Tech sector’s forward P/E is “nowhere near” the levels seen in the run-up to the dot-com bust.

Even the all-important cyclically adjusted price-to-earnings (PE) ratio, known as the Shiller PE ratio, didn’t reach dot-com levels during stocks’ late 2021 peak—although it remains above what was seen during the period before the Great Financial Crisis.

“In a nutshell, this is not a Dot-com Bubble 2.0 in our opinion, it's a massive over-correction in a higher rate environment that will cause a bifurcated tech tape with clear haves and have nots of tech,” Wedbush’s Dan Ives wrote in May 13 note. “There will be many tech and EV players that go away or consolidate, but we pick the winners from our vantage point.”

Ives called the recent downturn in tech a “generational buying opportunity,” even as other market experts urged caution.

Macroeconomic differences could lead to a deeper recession

The period surrounding the dot-com bust and today may be startlingly similar, but they also recall a perhaps apocryphal quote often attributed to Mark Twain: “History doesn’t repeat itself, but it often rhymes.”

Jeremy Grantham, the co-founder and chief investment strategist of Grantham, Mayo, & van Otterloo, a Boston-based asset management firm, emphasized the macroeconomic differences between the dot-com era and today’s markets in a CNBC interview this week. Tech stocks recent fall may be similar to what was seen in 2000, he said, but the outcome for the economy could be even worse today.

"What I fear is that there are a couple of differences with 2000 that are more serious. One of them is that the 2000 crash was exclusively in US stocks, bonds were great, the yields were terrific, housing was cheap [and] commodities were well behaved," Grantham said, noting that 2000 "was paradise" compared to now.

The legendary investor added that today, on the other hand, the bond market recently hit the “lowest lows in 6,000 years of history.” Additionally, energy, metal, and food prices are soaring, and the housing market is showing signs of cooling, which could present serious problems for the economy.

"What you never want to do in a bubble is mess with housing, and we're selling at a higher multiple of family income than we did at the top of the so-called housing bubble in 2006,” Grantham said. "We are really messing with all of the assets. This has turned out, historically, to be very dangerous.”

A Fed-induced recession

Experts say tech stocks’ recent collapse won’t be the key instigator of a recession like it was in 2000, however. Instead, the Fed’s attempts to fight nearly four-decade high inflation are expected to be the main source of economic pain.

The Federal Reserve has raised interest rates twice this year, once by a quarter-point in March and again by a half-point in May, and it’s likely to continue increasing rates throughout the year. That could be bad news for both Wall Street and Main Street.

“The punchbowl can't be sipped from for forever,” Ball said, invoking the famous metaphor coined by former Fed chair William McChesney Martin, who served from 1951 to 1970.

“With inflation now running very hot and not being transitory, the Fed will raise rates to crush inflation. It'll be doing the right thing, but that is probably what is going to cause a recession,” he added.

The idea that the Fed will likely be the culprit if a recession does come is now a widespread belief on Wall Street. Even former Federal Reserve Vice Chair Randal Quarles said the central bank will struggle to engineer a “soft landing” for the U.S. economy—where inflation is reigned in, but economic growth continues.

In Ball’s mind, that may not be the worst thing.

“I think, simply, with the long passage of high rates of growth and prosperity and GDP gains, we're entitled to a recession. The popping of the bubble will create an awareness of reason and logic that a cold shower brings about,” he said.

This story was originally featured on Fortune.com

By Will Daniel