Decentralized Finance (DeFi) is likely to have a significant impact on how banks operate in the future – and even has the potential to shift the structure of the whole financial system at a macroeconomic level. Before we discuss and substantiate this hypothesis, we would first like to introduce the core concept of DeFi.

Decentralized Finance or “DeFi” in short, is an umbrella term encompassing the vision of a financial system that functions without any intermediaries, such as banks, insurances or clearinghouses, and is operated just by the power of smart contracts. DeFi applications strive to fulfill the services of traditional finance (also coined as Centralized Finance, or just CeFi) – but in a completely permissionless, global and transparent manner.

DeFi applications could be at the verge of challenging traditional finance actors on various fronts

The vision of a new financial system accompanies the blockchain space since its inception. However, while it has been an aspirational dream for the blockchain community in the past, the vision of a new financial system has come some steps closer.

Since 2020, DeFi is growing at an astonishing pace and billions of USD have been put in the ecosystem. The growth is mainly led by applications (also denominated as protocols) that are built on the Ethereum blockchain. In the following, we give an overview of the actors in the DeFi ecosystem from an economic point of view, introduce the maturity stages of DeFi and explain the potential of DeFi to outperform the traditional finance system in the years to come.

Commercial banks

The primary business model of commercial banks is to accept deposits and to give loans to its clients. Borrowing and lending are an elementary cornerstone of an efficient financial system as holders of funds get an incentive to provide liquidity to the markets and in exchange earn a return on their otherwise unproductive assets.

DeFi protocols enable for the first time to borrow or lend money on a large scale between unknown participants and without any intermediaries. Those applications bring lenders and borrowers together and set interest rates automatically in accordance with supply and demand. Moreover, those protocols are truly inclusive, as anybody can interact with them at any time, from any location, and with any amount.

In fact, the recent hype around DeFi applications is largely driven by the advancement of borrowing and lending protocols, such as Compound. In contrast to traditional finance, loans in DeFi are commonly secured by over-collateralization. However, companies such as Aave are currently working on enabling uncollateralized loans similarly to traditional finance.

Investment banks and issuers of financial instruments

The business model of investment banks usually involves the advisory on financial transactions. Also, the creation or trading of complex financial products and the management of assets fall in the realm of investment banks. DeFi protocols are already offering similar products.

For instance, Synthetix is a derivatives issuance protocol, which enables the decentral creation and trading of derivatives on assets such as stocks, currencies, and commodities. Also, decentral asset management for cryptocurrencies is evolving. Yearn Finance, for example, is an autonomous protocol, which searches for the best yields in the DeFi space and invests automatically for its users.

Exchanges

The function of an exchange is to organize the trading of different assets, such as stocks or foreign currencies, between two or more market participants. Even the exchange of cryptocurrencies against fiat money (e.g. US Dollar) can be attributed to CeFi, as the regular holder of cryptocurrencies needs to use exchanges like Coinbase or Binance(which are centralized organizations) to swap a unit of a cryptocurrency against another.

Now, with the emergence of decentralized exchanges (DEX), holders of cryptocurrencies no longer need to leave the crypto space for swapping their tokens. A prominent example of a DEX is Uniswap. DEX are composed of smart contracts that hold liquidity reserves and function according to defined pricing mechanisms. Such automated liquidity protocols play a key role in the development of an independent decentralized ecosystem without any CeFi intermediaries.

Insurances

An important function of insurance is to smooth out risks and bring security for market participants. An example of decentralized insurance is Nexus Mutual, which offers insurances that cover bugs in smart contracts. Since everything is based on smart contracts in DeFi, vulnerabilities in the code of smart contracts is a fundamental risk for DeFi users. Decentralized insurances are still in their infancy, but it can be expected that a larger amount and more sophisticated insurance models have the potential to emerge in the DeFi space in the future.

Central banks

So-called stablecoins are based on blockchain protocols that have the principle of price stability inherently encoded and, thus, fulfill the function of a reserve currency. The introduction of stablecoins set the foundation of the functioning decentralized financial system, as they enable participants to engage with each other without the underlying risk of price volatility. There are three options how a cryptocurrency can reach price stability.

First, stablecoins can reach high degrees of price stability by pegging a currency to other assets. For example, for each issued unit of USD Coin a real US Dollar is held in reserve.

From a decentralized finance perspective, another interesting approach is the issuance of stablecoins by using other cryptocurrencies as collateral. A central protocol for the Defi ecosystem is Maker DAO, which issues the cryptocurrency DAI that is backed by other cryptocurrencies and ensures with its algorithm that the value of 1 DAI is hovering around the value of 1 US Dollar.

Thirdly, there are more experimental approaches that aim to reach price stability without the use of collaterals. For instance, the protocol Ampleforthautomatically adjusts the supply of token in accordance with demand.

Crypto-based finance has reached the next maturity stage, as it covers all basic functions of a financial system

We argue that DeFi has reached an important intermediate step to become a substitute for traditional finance solutions. While crypto-based finance solutions were merely capable of realizing efficient value transfers in the past, now the time value of money is reflected in crypto-finance.

Three maturity stages of a decentralized finance system

Stage 1: Efficient value transfers

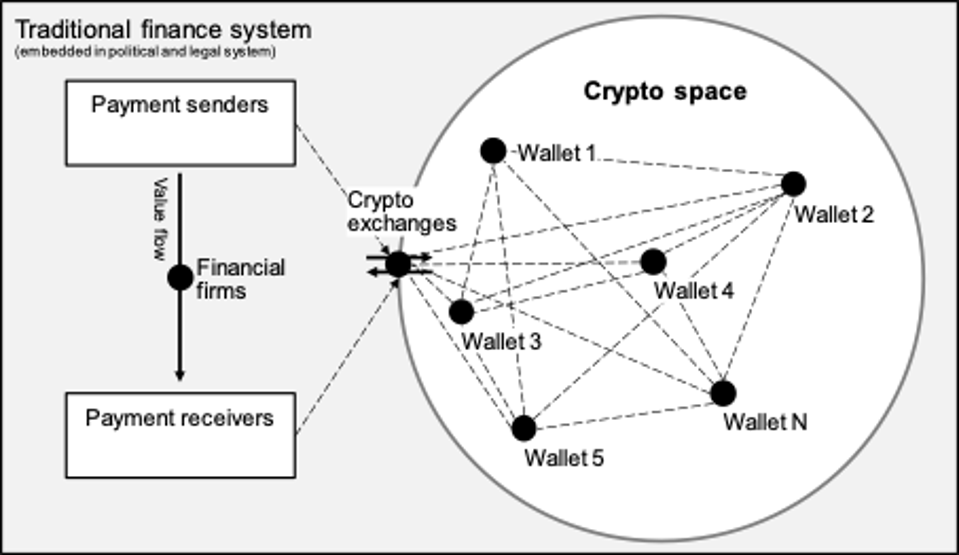

Until now, centralized exchanges and wallet providers have been the only successful blockchain business models at scale. The reason for the success of centralized exchanges is that they are the main entry point to the crypto space (see Figure 1). The common user needs to swap fiat money (e.g. US Dollar) against a cryptocurrency before being able to interact with services in decentralized finance. Furthermore, wallet applications are established that enable users to safely store and transfer their cryptocurrencies.

Based on those two applications, exchanges and wallets, efficient value transfers between unknown parties could be conducted for the first time without the need of traditional finance actors. This enabled the crypto space to fulfill limited functions of a financial system, namely speculation on (crypto) assets and the facilitation of payments. Thus, disintermediation of financial firms occurred – but only, if savers of traditional finance wanted to diversify their portfolio towards crypto assets or needed a frictionless payment system. We propose this to be the first maturity stage of a decentralized finance system.

Figure 1: First maturity stage - The crypto space as alternative for value storage and payments

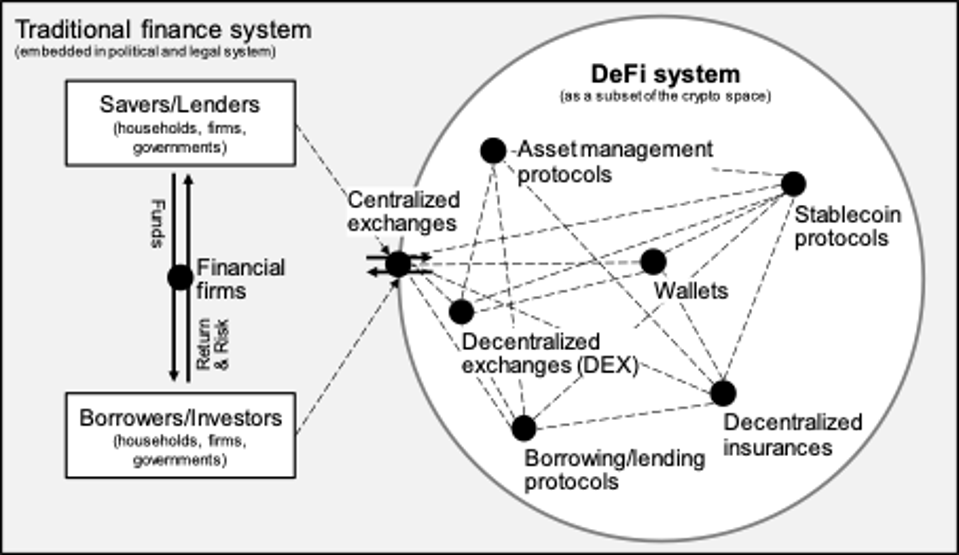

OWN ILLUSTRATIONStage 2: Connecting savers and borrowers

Still missing was the ability to deal with flows of funds from savers to borrowers and vice versa. In the following years, additional elements of a more advanced financial system were developed. The function of a payment system could be advanced with the development of stablecoins, decentralized exchanges, and borrowing/lending protocols. Thereby, DeFi developed the necessary platforms for facilitating the flows between savers and borrowers.

It might be no coincidence that the start of the explosive growth for the whole DeFi ecosystem could be observed with the advancement of the lending/borrowing protocol Compound. Since Compound started the distribution of its governance token, COMP, on June 15, 2020, the whole DeFi ecosystem showed a steep growth trajectory. Functioning lending/borrowing protocols, such as Compound, might have been the missing cornerstone for the foundation of a properly working decentralized financial system. This can be marked as the second maturity stage of the decentralized finance system.

Figure 2: Second maturity stage – Schematic illustration of the interplay between traditional ... [+]

OWN ILLUSTRATIONStage 3: Competing for traditional finance funds

DeFi can be described as a platform that is competing with traditional financial firms for the same resources. However, DeFi is an encapsulated system, which is not obeying the same rules as traditional finance. In particular, national law does not apply and regulatory policies can hardly be enforced in the DeFi space. This might be a major competitive advantage over the highly regulated traditional finance firms.

For example, financial innovations can be freely developed and implemented in DeFi without regarding regulatory boundaries. On the other hand, the absence of common legislative and political principles has certainly major disadvantages. It can be doubted that mainstream savers would consider the current DeFi environment a trustworthy destination to invest their pension. Hence, the crucial question for the advancement of DeFi to the next evolutionary stage will be:

- To which degree are savers of traditional finance willing to relocate their funds towards DeFi applications?

- To which degree are borrowers of traditional finance willing to access funds from DeFi applications?

To answer both questions at the current point in time: Only to a very limited degree. The reason is that most traditional finance savers or lenders do not trust the crypto space or simply do not know about DeFi. The influx of capital into DeFi applications since June 2020 most likely stems from idle assets on crypto wallets, i.e. from a redistribution of assets within the crypto space. Nevertheless, the rising use of DeFi protocols proves that the system is scalable and working. Today, the users of DeFi belong to the group of "innovators" or "early adopters" (i.e. a very small proportion of households). Tomorrow, the users might be mainstream households.

DeFi has the potential to outperform the traditional finance system in the years to come

We argue that there are three reasons why DeFi has the potential to outperform the traditional finance system and to gain increasing attention in scientific, economic, and public debates:

- Speed of growth: DeFi is a highly scalable and global ecosystem. Once DeFi as a whole (or a specific DeFi application) proves its utility, exponential growth is possible. The website DeFi Pulse monitors the total value locked (TVL) on smart contracts on all relevant DeFi applications (i.e. how much money has been poured into the ecosystem by its users). The increase of TVL between June and August 2020 illustrates powerfully the exponential growth potential of DeFi. While 1st of January 2020 the TVL was at $0.7 billion, it started skyrocketing in June 2020, reaching 1.9 billion 1st of July, 4 billion 1st of August, and surpassed the $8 billion mark 1stof September 2020.

- Room for growth: According to Messari, a crypto market analytics firm, the capitalization of all DeFi applications was just at 1.5% of the total crypto market as of July 2020. Therewith, it could be argued that there is a lot of room for growth only by further asset redistributions within the crypto space. Looking beyond the crypto space, lets us derive the real potential of DeFi. According to the Institute of International Finance, global household debt alone amounts to 48 trillion US Dollar in 2019. If DeFi covers just 0.1% of that debt, DeFi's TVL would grow by 500% compared to the beginning of September 2020.

- New market segments: According to The World Bank, 1.7 billion adults do not have access to banking services. DeFi is permissionless, meaning that anyone can access those financial services from anywhere in the world. In principle, just electricity, an internet connection, and smartphones are needed. DeFi could provide a viable option in regions, where banking services are too expensive compared to income, little trust in financial institutions persists, or if financial institutions are simply too far away. A prerequisite, however, for reaching unbanked adults is that DeFi applications develop more intuitive user interfaces and simplify the on- and off-ramp with fiat currencies.

Conclusion: Crypto-based finance is here to stay

For the first time in history, a financial system is developing without intermediaries at a large scale. So far, DeFi applications cannot compete in terms of security, speed, and ease of use with traditional finance solutions yet. But DeFi has produced real, working applications that have already managed to attract billions of capital. Those resources will be used to develop more competitive and user-friendly applications in the future.

Yes, there are parallels to the ICO hype of 2017, which resulted in a sharp increase and price crash across virtually all cryptocurrencies in 2018. Since then, the interest of mainstream media has diminished. However, it has been largely unnoticed that the influx of capital through ICOs has enabled the blockchain community to bring the technology to the next evolutionary stage. Now again, large sums are invested into blockchain technology. But in contrast to 2018, applications already have been developed and are running. While we might be standing at the verge of a new bubble, we might also be at the beginning of a new big development cycle for blockchain technology.

For sure, many more development cycles need to follow. However, it is not unrealistic to state that decentralized finance will be more efficient, convenient to use, and secure than traditional finance. It will be highly interesting to observe how the different actors in traditional finance will respond when profits start to deteriorate because of DeFi.

This article originally appeared on Forbes.