(Bloomberg) - In their crusade to get rampant inflation under control, the world’s major central banks risk fueling further chaos in bond markets that play crucial roles for the economies they’re trying to protect.

Policy makers, in a rush to rein in consumer prices, are quickly lifting interest rates and ending programs that made them the dominant buyers of government debt in places such as the US, Europe and Australia. Investors have yet to pick up the slack, helping create a liquidity drought that’s led to historic swings in yields in recent months.

“Worst we have ever seen,” is how Andrew Brenner, head of international fixed income at NatAlliance Securities, characterizes conditions in the bond market. “Central banks ruined liquidity from what it used to be.”

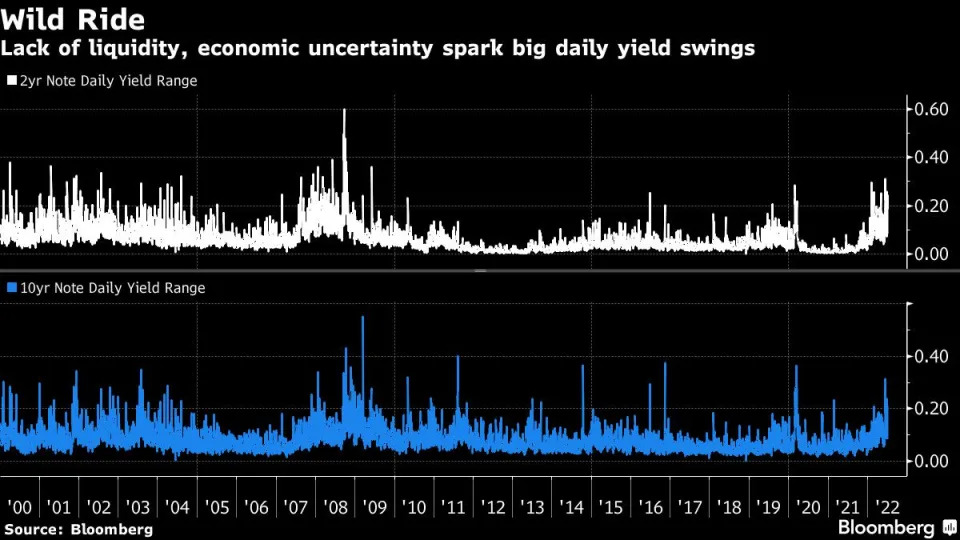

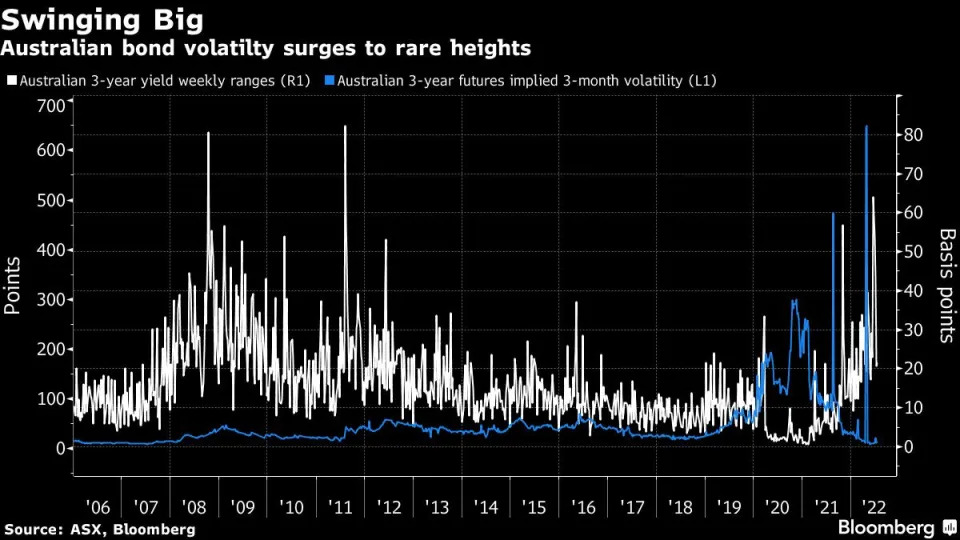

From Sydney to Frankfurt to New York, market weaknesses long hidden by ultra-easy monetary policies are being exposed, stoking concern about potentially painful disruptions that could ricochet into other markets and the economy as a whole. Once-boring German bunds are jumping around by the most on record, while Australian bond futures are near the most volatile in 11 years. Japanese bankers are grappling with days when not a single benchmark bond trades.

But it’s in the $23 trillion US Treasuries market where the dislocations are causing the most trouble, fueling angst from investors and regulators alike about what can be done to shore up this crucial global financial linchpin.

With US Treasuries serving as the risk-free benchmark for more than $50 trillion of fixed-income assets, extreme volatility in their yields could make it tougher for private-sector companies to raise capital easily and at the lowest possible cost. The market gyrations also threaten to introduce chaos into what traditionally has been the preferred asset class for pension funds, retirees and others looking for the safest possible investment returns. And all of this in turn could pose risks for the broader economy that eventually may force central banks to change their plans.

The European Central Bank is already working on a program to limit premiums on lower-rated government debt in the euro area. In the US, the lack of Federal Reserve purchase of Treasuries has handicapped trading -- and some dealers are even saying dislocations in money markets may put pressure on the Fed to scale back its plans to shrink its portfolio that had swollen to almost $9 trillion due to quantitative-easing bond buying.

“We are now seeing outsized intraday yield moves in the US as well as in European markets,” said Lawrence Gillum, a fixed-income strategist at LPL Financial. “If we start to see more cracks in markets, the Fed will be in a really tough situation -- because they will be trying to fight inflation on one hand and on the other trying to support the smooth functioning of the Treasury market.”

One issue that’s increasingly come into focus is the legacy of measures to strengthen the banking system in the wake of the 2008 global financial crisis. Tighter capital rules and restrictions on the use of leverage have made banks less willing to expand their government-bond trading capacity, hamstringing one of the market’s most-crucial sources of liquidity.

Aussie Angst

That wasn’t as much of an issue when central banks were sopping up the trillions of dollars of securities that governments were issuing to fund the battle against economic fallout from the Covid-19 pandemic. But a dearth of market making by banks is problematic now as the Fed and many of its counterparts scale down their debt holdings.

“The size of the market has grown quite substantially,” said Rob Nicholl, who heads the Australian Office of Financial Management, which oversees the country’s debt issuance. Without market-making capacity keeping up, “when you get periods of volatility, you are almost mathematically going to get periods where liquidity disappears more quickly.”

While concerns about bond-market liquidity have been percolating for years, the fears are indisputably coming to fruition in 2022. The dynamic is on display as intraday yield swings of more than 10 basis points become commonplace across most major markets.

A Bloomberg measure of Treasury liquidity is near its worst level since trading seized up in the spring of 2020 at the onset of Covid-19. Barclays Plc strategists highlight other metrics, including higher transaction costs.

In Europe, German bonds have been rocked by the highest volatility on record by some measures, as investors confront both an end to the ECB’s quantitative easing and a deeply uncertain rate-hike cycle -- all as trading volumes recede during the summer months.

That means the yield on a security could be drastically different between when an investor makes a trade and just moments later.

“Doesn’t matter if it’s outright levels, spreads or curves, all moves could be obsolete within minutes and see proper U-turns anytime,” said Jens-Christian Haeussermann, a government bond trader at Germany’s Commerzbank AG. “Liquidity drained dramatically.”

The wildness of trading in US bonds has unsettled some international investors -- an important group of buyers for American debt.

“What’s taking place recently are moves irrelevant to any news or events -- and that suggests players could be scrambling to cover positions,” said Eiichiro Miura, general manager of the fixed-income department at Nissay Asset Management Corp., a unit of Japan’s biggest life insurer.

Miura’s home market isn’t immune from liquidity challenges, though problems in Japan are centered on how much the Bank of Japan has bought rather than the end of purchases. One legacy of years of massive bond buying by the BoJ -- it now holds about half of the government bond market -- is that there’s just not much supply available for investors.

Japan’s bond buyers are finding it harder to complete transactions since any period outside the 2008 global credit crunch. There have been bouts of low volume in both the cash market for government securities and in futures. Sellers failed to deliver 3.53 trillion yen ($26 billion) of government bonds in June, the second-largest amount ever in BOJ data going back to 2001.

Similar problems are visible in Europe, and poised to get worse.

A regulatory measure that comes into force in September will compel hundreds of asset managers to post more collateral -- at a time when there’s less high-quality investments available to serve that role. Germany’s free float -- or the amount of its debt available to the general market -- is around record lows, according to Bloomberg Intelligence.

With risk-free securities more difficult to trade, it’s undermining the environment for the tens of trillions of dollars worth of assets that are benchmarked against them -- so-called spread products. Without incentives to big banks to add market-making liquidity, the risk is that costs will be borne by borrowers and investors across asset markets.

“While sovereign bond markets are still functioning very well, price makers’ appetite to hold any risk positions is much lower than normal,” said James Wilson, a senior portfolio manager in Melbourne at Jamieson Coote Bonds, which oversees A$4.3 billion ($3 billion). That’s been the case “especially for spread products -- leaving markets jumpy and prone to the very wide daily ranges we have seen lately.”

Despite the volatility, not everyone sees evidence of structural problems in global bond markets. Fed Chair Jerome Powell told lawmakers in June that the Treasuries market was functioning “reasonably well.” However, former Treasury Secretary Timothy Geithner is among those urging structural reforms to address liquidity issues as the Fed’s footprint in the market shrinks.

For Kevin McPartland, head of market-structure research at Greenwich Associates, it’s not clear if the bond market is “just broken” or if this type of action is simply what’s to be expected during an especially volatile period. Regardless, the situation invokes the old notion of “moral hazard” -- or the risk that aggressive policies of central bankers can distort market prices and eventually burn investors when they are reversed.

“It’s hard to take the punch bowl away,” McPartland said, referring to the withdrawal of loose monetary policy. “Everyone has gotten so used to the Fed backstop. It’s hard to say if the market needs it or has just grown accustomed to it. I really wonder about the moral-hazard idea.”

By Liz Capo McCormick, Garfield Reynolds and Greg Ritchie