(Beaumont Capital Management) With the relatively unprecedented strength we have seen in global equity markets over the past ~2.5 years (with one rather extreme hiccup in between), some investors may be apprehensive about investing in equity markets going forward. This age-old market-timing predicament appeals to both reason and natural emotional biases.

Emotionally, when you buy anything, it feels good to get a “good deal” and buying after large market run ups may not feel like a “good deal”.

From a more rational standpoint, it is incredibly disadvantageous to one’s financial future to invest at historic market tops such as those we saw in the Dotcom bubble and 2008.

While these historic events are certainly painful outliers, both data and market mechanics support investing at new highs or rather not “waiting for a better price.”

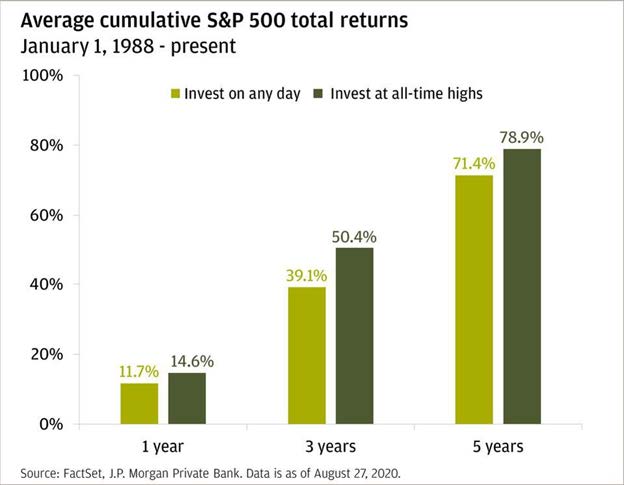

As the chart below shows, S&P 500® Index performance has historically been better going forward from all-time highs. This makes sense mathematically, as to go down 50% you must first go down 10% etc., but also logically because the natural state of the market is upward. While on a day-to-day basis the market’s performance is akin to a coinflip, 73% of one-year periods1 have been positive and the longer the investment period, the more likely the results are going to be positive.

Source: FactSet, J.P Morgan Private Bank, as of 8/27/20

Even if we ignore the opportunity cost of staying out of the market and waiting for a “dip”, market pullbacks aren’t necessarily guaranteed buying opportunities. Obviously if you buy at a cheaper price, you’ll have better returns all else equal. However, over the past quarter century, “buying the dip” hasn’t paid over the following year. Not to mention, emotionally, how does one make this timing decision of buying the dip—how big a dip will be required? How does one know if the dip will or will not turn into something much worse?

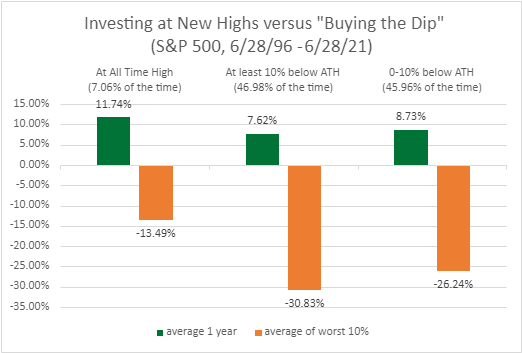

As outlined below, over the last 25 years, we see that investing at ATHs has actually been indicative of the best performance over the following year, while buying after a 10% or greater pullback has produced the worst performance. Perhaps most notably, by one measure ATHs have represented the safest time to invest with the worst 10% of one year periods after ATHs showing far smaller losses than in the other two scenarios.

Source: Koyfin, Beaumont Capital Management (BCM). Data for the period 6/28/1996 through 6/28/21.

Conversely, on average, large pullbacks represent the most dangerous time to be (or become) invested. This rather simplistic approach makes sense as usually things are going well when the market is making new highs and things are going poorly while it is falling. It also highlights some of the potential attractiveness of momentum-based strategies, which aim to capitalize on this relationship.

Ultimately, investors should not be fearful of investing at All-Time-Highs. Given that any equity investment comes with an implied return, being uninvested can be particularly painful—the market has always recovered from a drawdown but if you forego investing at an ATH, there is no assurance you’ll ever see a cheaper price. In addition, a good tactical strategy can further mitigate the strain on your portfolio (and your mind) when trying to invest in any market situation, given their ability to quickly increase or decrease risk as opportunities present themselves.