(3D/L) Momentum investing, buying what has been going up and selling what has been going down, is a paradox. It is easy to explain in terms of mechanics, and very hard to explain in terms of why it works. (And it does, more often than not, work.) Traditional economists, who start with the premise that investors are rational beings, find momentum particularly troubling. Not only does the success of such a simple strategy imply a grossly inefficient market, but if there is an effect, it should be that stocks that have been going up for a while are likely to be overpriced and so ought to be more likely to go down rather than up.

Not being economists, we do not spend a lot of time in search of a theoretical justification for momentum. If pressed, we will point to the work of the behavioral economists, who do not take as a given that everybody is all that rational. We believe that investors have a natural, and generally useful, tendency to temper their predictions of the future with recent observations of reality.

You might love a company and think that, in the abstract, its stock is worth $100 a share. But if it traded around $50 just the other week, today’s price of $60 may seem too high. So you wait a while until $60 seems normal, when you resume buying, until it hits $70, when you pause again to get used to the new level. If enough investors act this way you would see what we do see in the markets. Much loved stocks do not gap up suddenly, even on good news, as often as they march inexorably higher over time.

Of course, the effect also works in the downward direction, as a grim long-term view eats away at the current situation. We worry something similar is now happening with the closely related issues of inflation and interest rates.

Over the two years ending in January this year, the US money supply (M2) increased by about 41%. That is not completely unprecedented historically, but is far outside the experience of nearly every investor alive today. (Over the 30 years ended 12/31/2019, M2 grew by an average of 5.4% annually.) Mainstream macroeconomics texts are pretty clear that this level of increase in the money supply will likely result in inflation. Expecting consumer prices to rise by 41% is both simplistic and an exaggeration, but it is the right order of magnitude.

We have several times over the past two years used this commentary to lament that market consensus inflation expectations were too low. They have gone up some since, but not to a level consistent with a plain interpretation of the money supply data. When projections based on theory meet with actual recent experience, recent experience often wins out.

At the same time, there has been a steady progression, a momentum, in the inflation narrative. First there was no inflation. Then it was limited to a few items in short supply, then there was some general inflation, but small and transitory. And currently there is some not so transitory inflation, but the Fed is on the job, so it will be modest and short lived.

Speaking of the Fed, there has been a related and parallel momentum in interest rate expectations. With the exception of very recent speculation involving the Ukraine war, the expectations have been steadily climbing, but are still far below what a person might naively expect to go along with an inflation rate around 7%.

In the immediate aftermath of the Russian invasion of the Ukraine there was a surprising rally in equity markets. One of the proffered explanations was that economic stress from the war and related sanctions would cause the Fed to delay or slow rate increases. We agree that it will likely have that effect on the Fed but using that as an excuse to buy stocks strikes us as irrational. It is like a man being overjoyed at breaking his arm because it means the postponement of a root canal scheduled later that day. We are going to have the root canal sooner or later.

The invasion of Ukraine is itself another example of what causes momentum, in the sense of a failure to imagine very far from recent events and the status quo. With the hindsight of five days, it is obvious that it was a spectacularly ill-conceived operation. Putin planned on a short excursion involving a show of overwhelming force and perhaps a brief occupation of the capital, long enough to secure territorial concessions in the east and perhaps install a new Russia-friendly leadership.

This was a miscalculation based partly on Putin believing his own propaganda, that not being a real country Ukraine’s citizens had little in the way of nationalist feeling, but it must have also been based on an unspoken assumption that recent events and the status quo would continue. A similar invasion of Georgia in 2008 during the six-day long Russo-Georgian war, and Russia’s 2014 seizure of Crimea, successfully followed scripts similar to what was apparently intended this time. In neither case did the West impose meaningful sanctions.

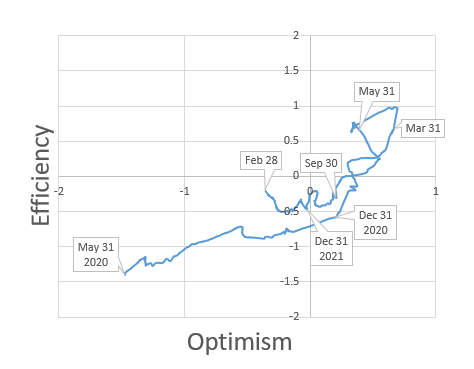

The Market Sentiment Framework

We use our Market Sentiment Framework to adapt the mechanics and weightings of our full quantitative models to changing market conditions.

The Sentiment Framework gauges the current state of market psychology on two dimensions. Efficiency measures the crowdedness of the market, the volume of participants seeking investment opportunities. Lower levels of efficiency imply more market mispricing. Optimism measures the willingness of investors to take on risk in exchange for distant anduncertain rewards. Higher levels of optimism imply a better outlook for risky asset classes.

Optimism continued its slow drift downward in February, while Efficiency rose slightly, while staying within the range it has inhabited for six months.

Optimism began the month at -0.19 and ended at -0.35. Although it has decreased steadily since mid-2021, Optimism is well above its pandemic lows seen in the first half of 2020.

Efficiency rose, starting the month at -0.50 and ending at -0.21. Efficiency continues to be comparatively low as compared to historical averages, which suggests a market that is still under stress.

Both measures are higher than where they were in early 2020, but have trended lower since spring 2021. The current positioning of the Sentiment Framework implies a market that is functioning less than ideally, with modestly optimistic but still fearful investors. This would imply a positive but challenged outlook for the market as a whole, but possibly an opening for value strategies to find opportunities.

Want to know more about the 3D/L sentiment framework as a way through the maze of "momentum" charts? It's as easy as taking a look at their Model Portfolio Strategist profile page.